- Rising commodity prices continue to support the inflation outlook while supply-chains are still exposed to disruptions, notably in China, and should continue distorting the global growth and inflation outlook leaving investors with higher-than-normal macro uncertainty.

- Monetary stimulus from the U.S. Federal Reserve (the “Fed”) and Bank of Canada (BoC) is getting removed at a quick pace to lean against excessive inflationary pressures. Rising rates should weigh on the growth outlook and equity valuation, but we do not expect a recession over the next 12 months.

- We downgraded equities to neutral while remaining underweight of fixed income and raising our cash allocation. On a regional basis, we upgraded U.S. equities to a small overweight. We remain overweight of Canadian equities and underweight to Europe, Australasia, and the Far East (EAFE) and Emerging Markets (EM) equities. We trimmed our underweight of bond duration to neutral as yields spiked. Overall, we continue to expect short-term market volatility.

- On a sector basis, we recently added an overweight to U.S. technology as play on Quality. Elsewhere, we remain overweight of U.S. financials, the energy sector, and the international travel sector.

The fishermen know that the sea is dangerous and the storm terrible, but they have never found these dangers sufficient reason for remaining ashore.

The Fed’s Narrow Path Between Growth and Inflation

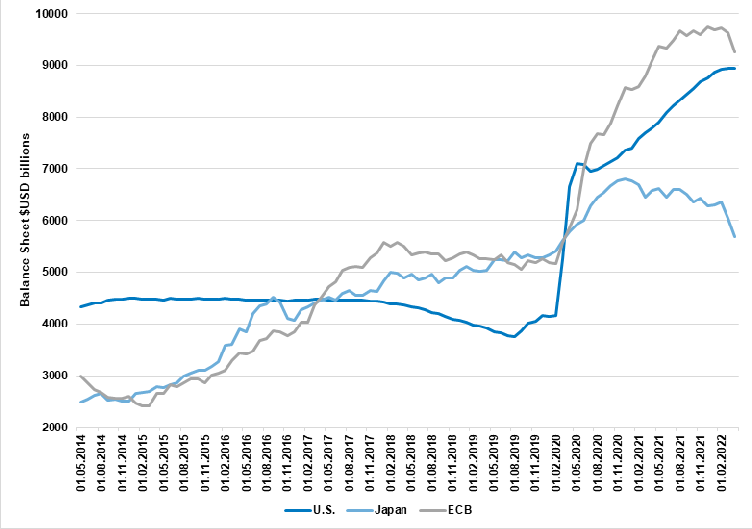

The Fed delivered its biggest rate hike since May 2000 by lifting its policy rate by 50bp to 1%. The decision was widely expected by markets while the language of Fed Chair Jerome Powell signaled that a quick march toward a neutral policy stance was necessary to bring down an inflation rate that is “too high”. Starting in June, the Fed will begin unwinding its balance sheet and increase the pace of reduction into September, at which time it plans to trim its $9tn balance sheet by $95bn per month. For major central banks including the BoC, quantitative tightening (QT) is already underway and is widely expected to accelerate during the year (Chart 1).

Chart 1: Revisions to 2022 Real GDP Growth Consensus Estimates Since September 1st, 2021

Source: Bloomberg, BMO Global Asset Management, as of May 5th, 2022

The earnings season delivered better-than-expected corporate revenues and earnings, especially in the U.S., led by strong performance from the Energy, Materials, Industrials and Healthcare sectors. Equities nevertheless struggled in April on i) rising rates and contraction of valuation multiples, and ii) increasing concerns that the Fed will fail to engineer a soft landing. Meanwhile, China continues to reel from the virus and the disruptive lockdowns imposed in several large cities, including Shanghai. Fear is also mounting that Beijing could face a similar path. China’s Zero-COVID policy is leaving the already fragile economy exposed to further weakness if the virus proves more difficult to eradicate than hoped by Chinese authorities.

Global Markets in April: Rising rates hurt

Bank of Canada: Oil-fueled hawks leading the hiking charge

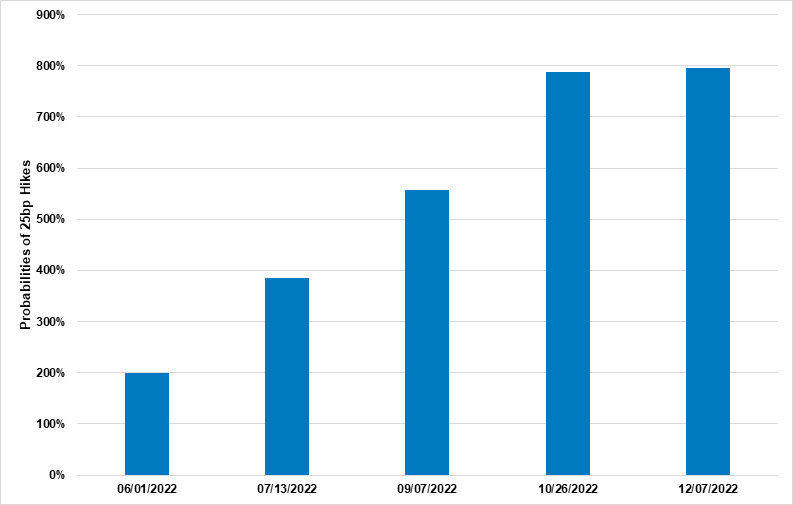

Although most developed economies are feeling the pain of high inflation, not every major central bank is ready to tackle inflationary pressures aggressively. For instance, the Bank of Japan is not showing any signs of hiking whereas the Bank of England, which recently hiked, is increasingly concerned about slowing economic growth. For Canada, we continue to expect above-trend growth into 2023, underpinned by a robust outlook for commodity prices and expectations that the housing market will cool from rising mortgage rates, but remain tight, especially with rising immigration levels. For the BoC, we think the path of rate hikes is likely to be less challenging than the Fed, which should support the loonie. After a 50 basis points (bp) hike in April, markets expect another 200bp of tightening by year end for the BoC, which would take the policy rate to 3%, the highest since 2008 (Chart 2).

Chart 2: BoC Market-Implied Hike Probabilities for 2022

Source: Bloomberg, BMO Global Asset Management, as of May 5th, 2022.

Equity Volatility: Tough year-to-date ride, but not out of the historical norm

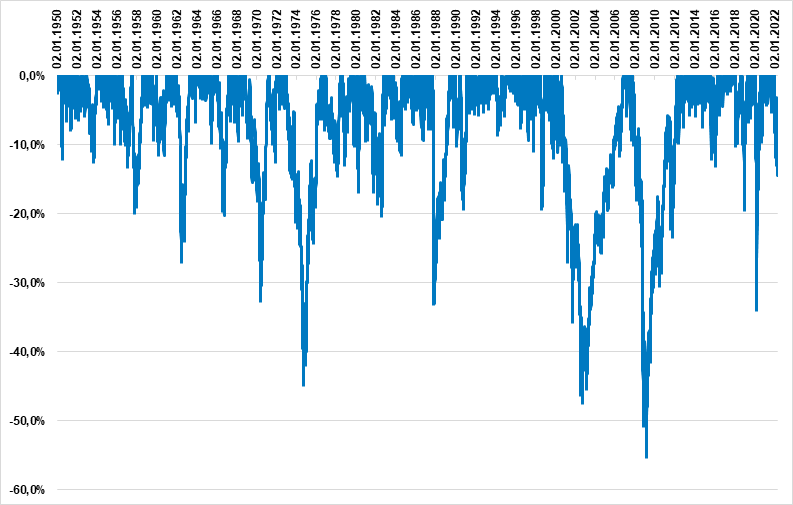

The Nasdaq is well into a bear-market this year and, at the time of writing, the S&P 500 is down nearly 15%. By comparison to the history since 1950, equity investors have been unusually fortunate in recent years, experiencing very mild and short-lived episodes of volatility and drawdowns, except for the 2020 lockdown storm (Chart 3). While the bond and equity pain has been significant this year, the much higher yields are leaving fixed-income assets in a much better shape for the future. We think investors should start warming up to bonds over coming months as yields reach higher levels. For equities, the 20% decrease in valuation (i.e., falling price-to-earnings (P/E) ratio) is leaving equities more attractively valued to long-term investors.

Chart 3: Historical Drawdowns for the S&P 500

Source: Bloomberg, BMO Global Asset Management, as of May 6th, 2022.

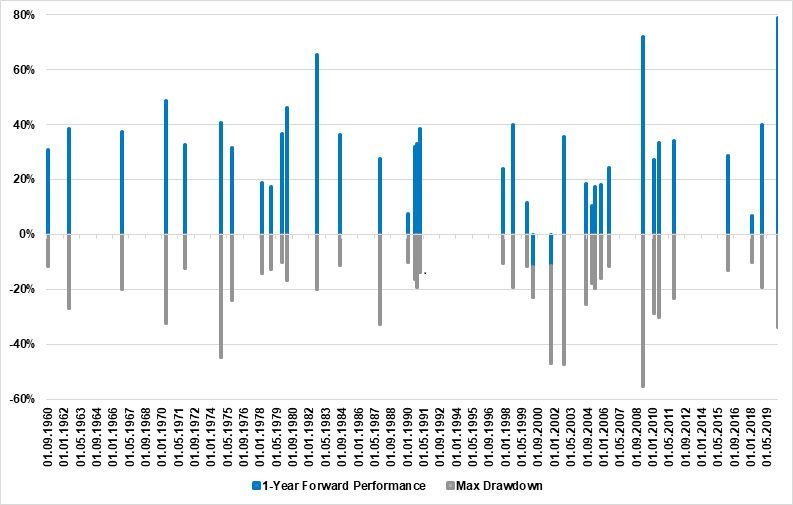

Although calling for market bottoms is not easy, the combination of excessive investor pessimism and more attractive valuations following sharp corrections such as the one we are currently experiencing tends to offer attractive investment opportunities. Looking at the largest (i.e., greater than 10%) S&P 500 drawdowns since 1950, we see that while investors should not expect to fully recover current losses over the next year, the ongoing equity pain is making it easier to expect positive returns from equities over the next year (Chart 4). At the very least, investors should warm up to equities as the storm brews and make plans to rebuild their equity exposure into the summer

Chart 4: Positive Performance Tends to Follow the Storms for the S&P 500*

Source: Bloomberg, BMO Global Asset Management, as of May 6th, 2022. * Note: 1-Year forward performance is calculated using daily total returns starting on the day where the 5&P 500 bottomed.

Outlook and Positioning: Stepping back to neutral on equities, upgrading U.S equities, expecting more headwinds for bonds

We continue to expect volatile markets as the Fed hikes and leans against inflation in 2022. Although the Fed aims for the proverbial soft-landing of the economy, we think the path between growth and inflation is narrowing, which is fueling the bearish market narrative of rising fear over a recession. While we see below 30% odds of a recession over the next twelve months, thanks to a tight labour market and healthy households and businesses balance sheets, we expect investor sentiment to remain lackluster despite evidence of a resilient U.S. economy and strong earnings.

Because of this backdrop, we downgraded equities to neutral but left bonds to an underweight, thereby increasing our cash allocation. Regionally, we upgraded U.S. equities to a small overweight while we maintain an overweight to Canadian equities and underweights on EAFE and EM equities. On a sector basis, we remain overweight of U.S. Financials, U.S. Energy, and International travel sectors. We recently added an overweight to large-cap U.S. technology (iShares US Technology ETF, ticker symbol: IYW). Within fixed income, we took our duration up to neutral.

Disclosures

BMO Global Asset Management is a brand name that comprises BMO Asset Management Inc. and BMO Investments Inc.

The viewpoints expressed by the Portfolio Manager represents their assessment of the markets at the time of publication. Those views are subject to change without notice at any time without any kind of notice. The information provided herein does not constitute a solicitation of an offer to buy, or an offer to sell securities nor should the information be relied upon as investment advice. Past performance is no guarantee of future results. This communication is intended for informational purposes only. The information contained herein is not, and should not be construed as, investment, tax or legal advice to any party. Particular investments and/or trading strategies should be evaluated relative to the individual’s investment objectives and professional advice should be obtained with respect to any circumstance.

The portfolio holdings are subject to change without notice and only represent a small percentage of portfolio holdings. They are not recommendations to buy or sell any particular security.

Forward-Looking Statements Certain statements included in this news release constitute forward-looking statements, including, but not limited to, those identified by the expressions “expect”, “intend”, “will” and similar expressions. The forward-looking statements are not historical facts but reflect BMO AM’s current expectations regarding future results or events. These forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations. Although BMO AM believes that the assumptions inherent in the forward-looking statements are reasonable, forward-looking statements are not guarantees of future performance and, accordingly, readers are cautioned not to place undue reliance on such statements due to the inherent uncertainty therein. BMO AM undertakes no obligation to update publicly or otherwise revise any forward-looking statement or information whether as a result of new information, future events or other such factors which affect this information, except as required by law.

®/™Registered trade-marks/trade-mark of Bank of Montreal, used under licence.