2022 proxy voting season1 highlights

6,836

19%

53%

- Proxy voting is a key element of our stewardship and responsible investment approach. This piece summarizes how we voted in the Canadian market during the 2022 proxy voting season — a year that saw an unprecedented number of environmental and social proposals.

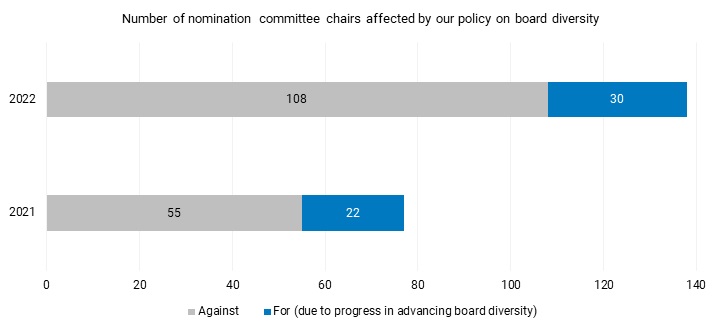

- Canadian board gender diversity saw some progress; we were able to support nearly 51% of the 55 nominating committee chairs we previously voted against in 2021, despite increasing our expectation that there should be at least 30% female representation on boards in 2022.

- At the same time, our vote guideline requiring at least one ethnically diverse director on boards went live for the first time in 2022, nearly doubling the number of nominating committee chairs we withheld voting for due to board diversity concerns.

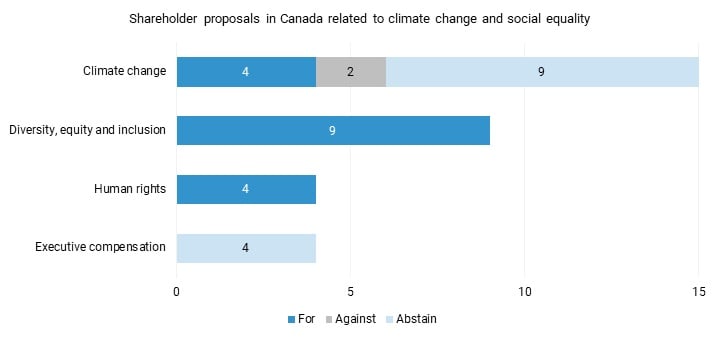

- We also supported around 53% of shareholder proposals related to climate change and social equality.

This past proxy season saw an even larger volume of shareholder proposals filed at North American companies compared to last year. In the United States, the number of environmental and social-related (E&S) shareholder proposals that came to vote nearly doubled. This was due, in part, to the U.S. Securities and Exchange Commission (SEC) loosening restrictions around the filing of such resolutions at the end of 2021 and not granting as many “no-action” requests from companies, which would have allowed them to exclude proposals from their proxy statements. While overall support for E&S proposals slightly dropped, those requesting racial equity audits received record approval, with 8 out of 22 passing. BMO Global Asset Management (BMO GAM) generally supported proposals calling for racial equity audits.

Canada had no regulatory changes related to filing shareholder proposals, but it was still a record year. We voted on 32 shareholder proposals related to climate action and social equality — an overall increase from 12 in 2021. We expect this trend to continue over the years to come.

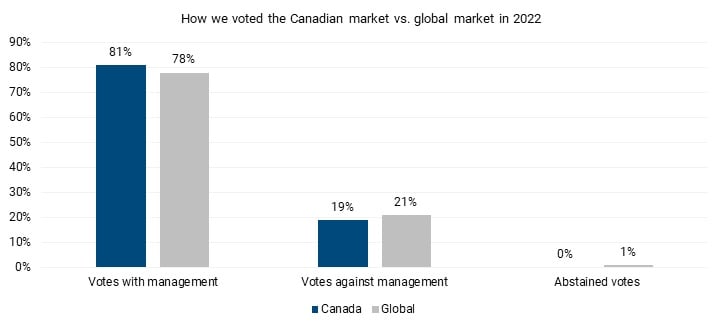

Our voting decisions are directed by our Corporate Governance Guidelines, which are reviewed annually to reflect industry best practices. We voted against management on roughly 19% of Canadian proposals during the 2022 proxy voting season — which was similar to our global average of 21% and suggests room for improvement across all markets in aligning objectives between shareholders and management on good governance. We also had at least one vote against management in nearly 80% of the meetings we voted.

As a result, we actively engaged with our portfolio companies during the season to seek a mutual understanding of good governance practices by conveying our expectations and vote intentions. In 2022 we engaged with 110 investee companies in advance of and the during proxy season to socialize our expectations and encourage good practices.

Board diversity

We raised our expectations for 2022 on gender diversity to a minimum of 30% from 25% female representation on the board. This is consistent with our 30% Club Investor Group Canada membership and commitment as a signatory to the Canadian Investor Statement on Diversity & Inclusion. We also implemented a voting guideline to withhold support from chairs of nominating committees in the absence of racial diversity — unless the board had conveyed meaningful plans, targets, and timelines to address the matter.

While we recognize sensitivities around assessing individual director identities, we encourage boards to report aggregated data on the number or percentage of racial and other types of diversity based on voluntary self-disclosure. Although still in its infancy, we believe that regulations and company practices will continue to evolve to enhance disclosures on diversity that are both relevant and comparable to peers.

During the 2022 proxy voting season, we withheld support for 108 chairs of nominating committees due to our guideline updates on diversity — almost twice as many as the same timeframe the year before. However, we supported nearly 51% of the 55 companies we voted against in 2021, suggesting increased alignment between shareholders and management on the benefits of achieving board-level diversity.

Compared to last year, we also increased our support for the number of nominating committee chairs to 30 from 22, where the board did not meet our expectations but demonstrated positive momentum in advancing diversity. This includes the addition of a female director and setting robust, time-based targets that look beyond gender.

Environmental and social shareholder proposals

We will generally support E&S proposals that call on companies to improve their business strategy and public disclosures on managing material environmental and social risks in line with recognized international standards and frameworks. Elements we consider in our assessment:

- Does the shareholder proposal’s ask/address a material or salient ESG issue for the company or a systemic risk for its industry?

- How does the shareholder proposal align with BMO GAM’s priority areas on Climate Action, Social Equality and overall good governance?

- How is the company performing against peers?

- Can the shareholder request be reasonably implemented?

This proxy season, we supported roughly 53% of shareholder proposals in Canada related to climate change and social equality. More specifically, we voted in favour of proposals that sought enhanced disclosures on climate strategy and targets, human rights due diligence and diversity in the workforce.

For example, we were supporters of a shareholder proposal filed at Constellation Software that called on the company to conduct a thorough review of racial equity in its workforce and disclose findings to shareholders. The proposal received 63% shareholder support and is one of the first related to racial equity to pass in Canada. We also supported shareholder proposals asking companies to advance Indigenous reconciliation initiatives at Toromont Industries and Onex Corporation. Toromont’s board recommended that shareholders vote in favour of this proposal, and as such, it passed with over 99% shareholder support. Onex opposed the proposal, and with 16% votes in favour (which included over 45% support from independent shareholders) did not pass.

We expect to see similar proposals filed in the future as shareholders seek meaningful disclosures on the effectiveness of companies’ initiatives in advancing Indigenous reconciliation and diversity, equity and inclusion.

Case study: Loblaw Companies Limited

As part of our engagement cycle during the proxy voting season, we spoke to Loblaw on its 2022 agenda items, including a shareholder proposal requesting the publication of its supplier audit results. The company had noted in our call that it intends to provide additional disclosure on this topic in the future which we encouraged.

Overall, we believe that the supplier audit results can provide better insight to shareholders on supply chain-related risks and consider the proponent’s request reasonable, given it aligns with what Loblaw intends to release in the near future. At the same time, it doesn’t constrain the company to a certain deadline or specify the content that should be included in the report. We voted in favour of the shareholder proposal to demonstrate our support for Loblaw’s intentions.

In certain cases, we opted to abstain on shareholder proposals where we agreed with the intention but found the request was overly prescriptive or not reasonably implementable. In our view, management should have more discretion in applying a suitable approach to address the particular ESG topic raised.

In our view, a robust climate action plan would remain relatively consistent each year, and an annual vote could create onerous work for shareholders in combing through these documents to look for changes. In this case, we would have considered a vote every two to three years more appropriate, given the consistency required. Like all shareholder proposals, we also consider companies’ willingness to engage on certain ESG issues, such as climate change, in our voting decisions, as well as the robustness of current climate strategies and disclosures.

Looking ahead to 2023

This year’s increase in environmental and social-related shareholder proposals highlights growing shareholder expectations on how companies manage different areas of ESG, such as climate change and social inequality.

As members of the Climate Engagement Canada (CEC) initiative — where we also serve on the Steering Committee — we will incorporate future CEC research and engagement outcomes into our assessment of companies’ progress towards net-zero commitments. Ultimately, this will inform our voting approach. In addition, we will continue to use internal methodologies and data from the Transition Pathway Initiative and Climate Action 100+ in our assessments. We will also consider how income inequality can be integrated into the evaluation of executive compensation packages, where we will encourage companies to disclose more information on how potential pay disparities are being addressed.

As we look ahead, we will continue raising our expectations on how companies manage material ESG risks. We will also continue to engage with our portfolio companies to gain feedback and align expectations to form a mutual understanding of good governance practices.

Disclosures

BMO Global Asset Management is a brand name that comprises BMO Asset Management Inc. and BMO Investments Inc.

The viewpoints expressed by the Portfolio Manager represents their assessment of the markets at the time of publication. Those views are subject to change without notice at any time without any kind of notice. The information provided herein does not constitute a solicitation of an offer to buy, or an offer to sell securities nor should the information be relied upon as investment advice. Past performance is no guarantee of future results. This communication is intended for informational purposes only. The information contained herein is not, and should not be construed as, investment, tax or legal advice to any party. Particular investments and/or trading strategies should be evaluated relative to the individual’s investment objectives and professional advice should be obtained with respect to any circumstance.

The portfolio holdings are subject to change without notice and only represent a small percentage of portfolio holdings. They are not recommendations to buy or sell any particular security.

Forward-Looking Statements Certain statements included in this news release constitute forward-looking statements, including, but not limited to, those identified by the expressions “expect”, “intend”, “will” and similar expressions. The forward-looking statements are not historical facts but reflect BMO GAM’s current expectations regarding future results or events. These forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations. Although BMO GAM believes that the assumptions inherent in the forward-looking statements are reasonable, forward-looking statements are not guarantees of future performance and, accordingly, readers are cautioned not to place undue reliance on such statements due to the inherent uncertainty therein. BMO GAM undertakes no obligation to update publicly or otherwise revise any forward-looking statement or information whether as a result of new information, future events or other such factors which affect this information, except as required by law.

®/™Registered trademarks/trademark of Bank of Montreal, used under licence.